Written by

Australian Dog Lover

17:01:00

-

0

Comments

“Medical treatment available to dogs and cats is now on a par with human health. Although this is a good thing, the cost of providing these treatments is expensive. Since there is no Medicare and no safety net, pet insurance makes sense financially for pet owners and the wellbeing of their pets”says Greg Mattes from Bow Wow Meow Pet Insurance.

"Our mantra is look after them, protect yourself" comments Natalie Carpenter from Petinsurance.com.au and that's exactly why we think it's vital for every loving pet parent to have pet insurance."

“Pet insurance can be an effective way to make sure you have the money available to pay for vet fees if the unexpected were to happen" according to Liz Walden from PetSecure. "As with humans, we simply don’t know when an accident or illness may strike, and so it makes sense to be prepared, so you are not faced with difficult decisions or financial difficulty if your pet were to have an accident or get ill."

The Cost of Pet Insurance

Choice Magazine (April 2014) compared premiums and benefits from a range of providers, and reported that premiums for dogs average around $390 for common breeds, but for more high risk breeds (e.g. Bulldogs), the accident and illness cover averaged at around $550 a year.

Natalie Smith from compareinsurance.com.au says that “whilst pet insurance can seem like an extravagance, it may save you a huge financial and emotional burden further down the line. Considering the exorbitant cost of vet bills, pet cover can literally save you thousands of dollars”.

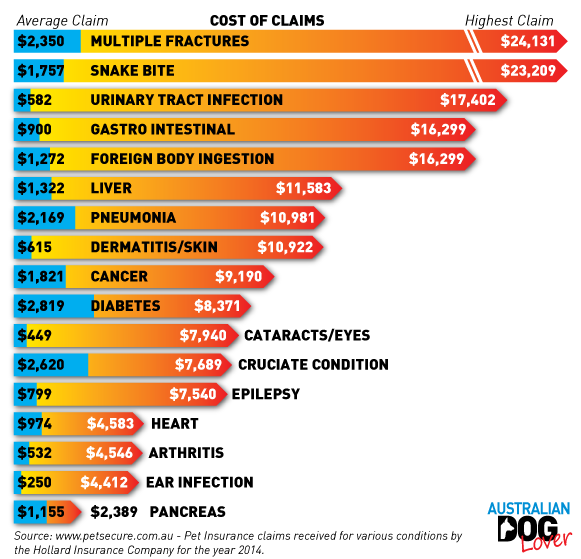

HCF Pet Insurance research shows that “1 in 3 pets are likely to need urgent veterinary care each year with the average claim over $1,000 and it is not uncommon for bills to exceed $10,000."

Sadly, an estimated 6,000 pets are put down each year because their owners can't afford the lifesaving vet care they require*.

Just this month I read the heartbreaking story of a young Pug who suffered from heat stroke and collapsed upon returning from his usual walk on a hot and humid day. Its owners were advised by the emergency vet that the treatment could cost $3,000 a day for up to 3 weeks. This still only offered a 50/50 chance of survival and not having pet insurance they took the devastating decision of putting him down.

Is Pet Insurance for Everyone?

Greg Mattes admits that "pet insurance may not suit every pet owner. If you have a pet that has had many medical issues in the past, it may not make sense to insure them as their policy would include many pre-existing conditions, which won’t be covered by pet insurance”.

His recommendation, along with all pet insurers we spoke to, is to “insure a new puppy or kitten from a young age to avoid any issues with pre-existing conditions”.

To put pet insurance costs into perspective, Bankwest’s Family Pooch Index revealed that, on average, owners will spend more than $25,000 over the lifespan of their dog.

"All pets can suffer from unforeseen illnesses and injuries." says John Cail from Petplan Insurance." From skin allergies, arthritis and gastro through to cruciate ligament injuries, lumps or being hit by a car - pets often require unexpected veterinary care."

HCF Pet Insurance advises that “with a choice of accident-only cover, accident and illness cover and premium cover, pet owners are now able to choose a policy that suits their needs and their budget. As with all other forms of insurance, the trick is to read the fine print. Knowing what your canine friend is covered for, can help avoid nasty surprises down the track”.

Are there alternatives to Pet Insurance?

Liz Walden says that “those who are disciplined can set up a savings plan by putting a bit of cash aside each month to cover a rainy day. A credit card with available credit is another option (albeit an expensive one), and nowadays we see people crowd funding – but that is by no means a guaranteed way to ensure your vet fees are paid.”

Greg Mattes gives a typical example based on an average claim of $3,000 to cover the expenses of a Cruciate Ligament procedure. If you're using a Credit Card, Loan or a Vet Pay facility you could be adding up to 30% to your bill and may end up spending a total of $3,935.

In that scenario, a pet insurance holder on their top level of cover would have seen $2400* paid in benefits after a co-payment of 20% (or $600).

* This scenario is based on a $12,000 annual level of cover and an average policy cost of $380/year.

Natalie Carpenter believes that "pet insurance is still the most simple and cost-effective solution".

What to look out for when comparing pet insurance policies?

“Just as you research your personal health insurance, you should always research your pet’s health insurance to make sure it suits their needs” says Nathan Crothers, Manager of Medibank Pet Insurance. “Key things to investigate include whether there is a co-payment and excess on the policy; what is the maximum annual benefit payable and what are the waiting periods that may apply”.

Natalie Smith explains "this is a time you must wait once you've bought a policy before you can make a claim. It exists to protect insurers from pet owners finding out that their pets are ill, or have become injured and only then want to buy cover."

She also warns against a practice called “double dipping” where some insurers charge an excess as well as limit the percentage of the vet’s bill that is payable.

She advises to check “what discounts are available and the period for which they apply as long-term discounts are generally better value than once off discounts or free cover special offers”.

Greg Mattes says that "if your pet has a known pre-existing condition (i.e. before you started your insurance policy) then it will not be included in your policy cover. However, once you’ve held continuous cover with us for 18 months and providing that your vet has verified that your pet is now free of any clinical signs of recurrence of that pre-existing condition you will be able to apply for an exclusion waiver”.

John Cail from Petplan encourages owners to "check if they will be covered if their dog damages property or bites someone" (called Third Party Liability) or if "they lose their pet through theft or straying".

Also check if your insurance policy will cover items like dental treatment or emergency boarding fees.

Greg Mattes says that "if your pet has a known pre-existing condition (i.e. before you started your insurance policy) then it will not be included in your policy cover. However, once you’ve held continuous cover with us for 18 months and providing that your vet has verified that your pet is now free of any clinical signs of recurrence of that pre-existing condition you will be able to apply for an exclusion waiver”.

John Cail from Petplan encourages owners to "check if they will be covered if their dog damages property or bites someone" (called Third Party Liability) or if "they lose their pet through theft or straying".

Also check if your insurance policy will cover items like dental treatment or emergency boarding fees.

Most pet insurers now provide cover options that include benefits paid towards routine or preventive care such as annual vaccinations, heartworm treatment, desexing etc.

Why is there an age limitation applying to illness covers?

Nathan Crothers adds that “as pets age, the likelihood of age-related illnesses such as cancer, arthritis or diabetes increases – which in turn increases the amount of benefits we pay out to our members”.

Natalie Carpenter comments that "we try and encourage people to get cover when their pets are puppies and with this in mind, we developed a unique puppy cover product".

Liz Walden advises that “provided that you did take out illness cover before your pet is 9 years of age, it will continue to be covered for illness for as long as you choose to keep your policy. We do not offer illness cover to pets over 9 years of age as the premiums would be cost prohibitive.”

What are the issues around specific conditions?

We found that most insurers will pay benefits towards the treatment of the deadly paralysis tick. Depending on the insurer and your chosen annual level of cover, you could receive benefits ranging from $500 to $1,000. Premium policy holders with both HCF Pet Insurance and Medibank Pet Insurance can receive up to $1,200 back for veterinary costs relating to the treatment of paralysis ticks.

Petplan's policies feature no sub-limits on specific conditions such as paralysis ticks.

Please remember this will fall way short of the thousands of dollars it could cost you at the vet with no guarantee that your pet will pull through. The safest option remains to use tick prevention treatments (on the Eastern seaboard) all year round to avoid the heartache of losing your pet.

HCF Pet Insurance offers two levels of covers and a range of optional extras meaning that you can design a policy that suits your pet’s life stage and needs. Depending on your chosen level of cover , you can receive up to 80% back on your dog’s eligible vet bills. HCF members will also save 10% on the cost of pet insurance.

Similarly Medibank Pet Insurance and ahm reward their Private Health members with a 10% discount on their premium and also offer a 5% multi-pet discount when insuring a second pet.

Bow Wow Meow Pet Insurance recently launched a program aimed at new puppy owners (run at this stage exclusively through vet clinics), which delivers benefits such as a free pet ID tag, a puppy guide e-book and discounted insurance offer. They also place the emphasis on responsible dog ownership with their new Breed Selector online tool.

Petinsurance.com.au recently launched a market first with a puppy cover product that "provides pet parents the comfort of knowing their premiums will stay the same for 3 years - with a guaranteed offer of renewal at the end of that 3-year period."

PetSecure offers a 10% discount for pensioners, rescue and service pets. These discounts will apply for as long as your policy is kept continuously. Also included is a free pet ID tag.

Petplan includes Third Party Liability as a standard benefit in all their dog plans, which will help cover you if your dog bites a stranger at the park or destroys someone's property.

They also give owners the option to include Death Cover as an extra benefit in their policy (it is standard in their Covered for Life Ultimate plan).

In Summary

As with everything, we found that generally speaking, you get what you pay for. If a policy is low cost, it is essential that you check the benefits and limitations that come with that price.

"You should focus on the positives of pet insurance and what it will cover, not on the uncovered items!" concludes Liz Walden.All pet insurance companies must provide a PDS (product disclosure statement) and we recommend that you check the fine print for any exclusions, restrictions etc. There is little point blaming your insurer for not paying out a claim when all the information is clearly outlined in their policy documents.

Please remember that you have a full 21 days (known as the cooling off period) from your policy commencement date to make sure that you are satisfied with every aspect of your chosen policy.

Thanks to new pet insurance comparison websites, customers are now able to check user generated (independent) feedback to help them make an informed decision on their cover.

Dogs are now considered part of our family and owners have come to expect higher levels of care from their pet insurance companies. Combined with increased competition in this market it can only speed up that process delivering more positive outcomes for our pets.

Thanks to new pet insurance comparison websites, customers are now able to check user generated (independent) feedback to help them make an informed decision on their cover.

Dogs are now considered part of our family and owners have come to expect higher levels of care from their pet insurance companies. Combined with increased competition in this market it can only speed up that process delivering more positive outcomes for our pets.

No comments

Post a Comment